Industry Overview

As laser-based technologies proliferate in defence, industrial, medical and research sectors, the demand for specialised eyewear capable of mitigating ocular hazards is accelerating. The Laser Defense Eyewear market is a compelling example of how protective solutions and risk-mitigation strategies are merging with advanced materials and green-technology awareness. Organisations are increasingly integrating eyewear that not only protects but aligns with sustainability and ergonomic trends, reflecting a broader shift towards energy-efficient manufacturing, worker wellness and regulatory compliance.

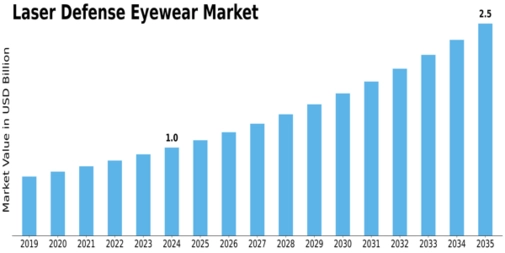

Market Outlook

According to the MRFR analysis, the global Laser Defense Eyewear Market was valued at USD 1.04 billion in 2024 and is projected to reach USD 2.495 billion by 2035, representing a compound annual growth rate (CAGR) of 8.28% for the period 2025-2035. The forecast suggests a robust expansion driven by rising awareness of laser hazards, increasing adoption of laser systems across sectors, and regulatory pressures. In this context, protective eyewear becomes a core component in sustainable workplace safety strategies.

Key Players

Key manufacturers shaping the market include Honeywell International Inc., 3M Company, Revision Military, Oakley, Inc., Bollé Safety, Smith Optics, ESS Eyewear, Pyramex Safety, and Radians, Inc.. These brands are investing in innovations around lens coatings, lightweight frames, and smart eyewear integration, aligning with both performance and sustainability objectives.

Segmentation Growth

By Application: The military segment leads the market thanks to defence requirements; the medical application is emerging fastest, due to increasing laser-assisted procedures.

By Product Type: Laser safety glasses dominate, given their widespread use in manufacturing and defence; goggles are growing rapidly in research and healthcare settings.

By End-Use: The defence end-use segment holds the largest share; meanwhile healthcare (including medical and surgical laser applications) shows the fastest emerging growth.

By Material: Polycarbonate remains dominant due to its lightweight, impact-resistant properties; glass is gaining traction due to clarity improvements and advanced coatings.

Regional growth: North America leads (USD 0.48 billion in 2024), followed by Europe (USD 0.34 billion) and Asia-Pacific (USD 0.15 billion) – with APAC as the fastest growing.

Conclusion

For organisations looking to adopt protective eyewear solutions, theLaser Defense Eyewear market Size offers promising opportunities. The interplay of advanced materials, safety regulations, ergonomic design, and sustainability (e.g., lighter frames, fewer replacement cycles) underscores its importance. Given the projected CAGR and market size doubling by 2035, manufacturers and users alike should prioritise adoption of certified, high-performance eyewear to meet risk mitigation and compliance goals.